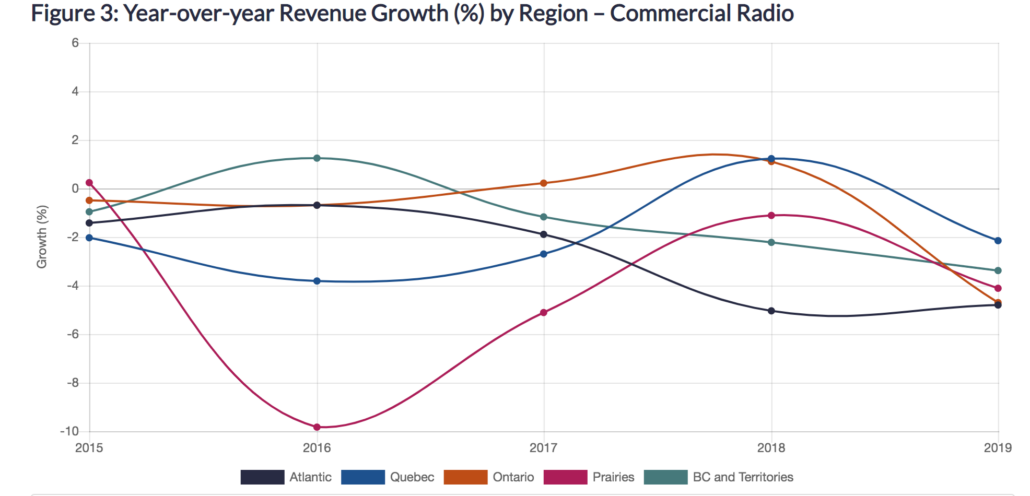

The CRTC’s recently-released 2019 Broadcasting Financial Summaries reveal growth in annual conventional television revenue for the first time in eight years, while commercial radio reported its largest year-over-year revenue decline in five years. Total broadcasting revenues declined by 1.3% between 2018 and 2019. The biggest drop in revenue was from CBC conventional television, as its stations collectively reported a decrease of $116 million (or 12.2%). Commercial radio stations reported negative annual growth of -3.9%, the largest year-over-year decrease in the past five years. None of the regions recorded positive growth with stations in Atlantic Canada reporting back-to-back declines of 5%. Lethbridge, Medicine Hat and Red Deer were the worst performing markets in the country, posting negative growth rates of 15.9%, -13.6%, and -11.8% respectively. Victoria, BC was the only designated market to report a positive growth rate in all of Canada (1.2%). Looking at commercial television, conventional stations reported revenues of $1,554 million in 2019, compared to $1,541 million in 2018. A year-over-year increase of 0.8% was mostly due to a 3.6% increase in national time sales. Quebec was the only region to post a year-over-year revenue decline (-4.4%) while the Atlantic region posted the highest growth (8.1%). Read more here.

The CRTC has called for comments on its proposal for a standardized approach to monitoring linear community channels and on-demand community programming services as part of efforts to establish consistent practices. The deadline for the submission of comments is Aug. 17.

![]() The Competition Bureau is investigating whether Videotron employees artificially boosted positive online reviews of its Helix IPTV platform and other products by posing as customers. The allegations, which haven’t been proven, date back as far as 2012 and are contained in a federal court affidavit filed by the bureau. Bell was fined $1.25 million in 2015 following a similar investigation.

The Competition Bureau is investigating whether Videotron employees artificially boosted positive online reviews of its Helix IPTV platform and other products by posing as customers. The allegations, which haven’t been proven, date back as far as 2012 and are contained in a federal court affidavit filed by the bureau. Bell was fined $1.25 million in 2015 following a similar investigation.

The Competition Bureau has submitted its final submission to the CRTC’s review of mobile wireless services, finding that even with the widespread introduction of “unlimited” cell phone plans, more Canadians could save money on their cell phone bills if Bell, Rogers and Telus faced greater competition from regional carriers like Freedom Mobile and Videotron. The bureau’s analysis found that prices are more than 50% lower for all cell phone users in markets where there is strong competition from regional carriers. The bureau continues to recommend that the CRTC pursue a Mobile Virtual Network Operator (MVNO) policy where Bell, Rogers and Telus would sell temporary access to their wireless networks to regional carriers who intend to invest and further expand their own networks. Read the bureau’s executive summary here.

Rogers Communications posted a total revenue decrease of 17% in Q2 and a 50% drop in Media revenue, reflecting the impact of the COVID-19 lockdown. Revenue decreases in the quarter were largely driven by 13% and 17% decreases in Wireless service and equipment revenue, in addition to the sharp decline in Media revenue. The Wireless service revenue decrease was mainly a result of lower roaming revenue due to travel restrictions and lower overage revenue, as a result of the continued adoption of Rogers Infinite unlimited data plans. Wireless equipment revenue decreased as a result of lower gross additions and device upgrades by existing subscribers during the pandemic. Media revenue declines were primarily the result of lower advertising revenue due to softness in the market and the loss of sports revenue, including at the Toronto Blue Jays. Media adjusted EBITDA decreased by 149% or $107 million, partially offset by lower programming and sports costs associated with the suspension of major sports leagues. Cable revenue decreased by 3% as a result of declines in legacy television and home phone subscriber bases, offset by growth in Ignite TV and internet subscriptions.

Rogers Communications posted a total revenue decrease of 17% in Q2 and a 50% drop in Media revenue, reflecting the impact of the COVID-19 lockdown. Revenue decreases in the quarter were largely driven by 13% and 17% decreases in Wireless service and equipment revenue, in addition to the sharp decline in Media revenue. The Wireless service revenue decrease was mainly a result of lower roaming revenue due to travel restrictions and lower overage revenue, as a result of the continued adoption of Rogers Infinite unlimited data plans. Wireless equipment revenue decreased as a result of lower gross additions and device upgrades by existing subscribers during the pandemic. Media revenue declines were primarily the result of lower advertising revenue due to softness in the market and the loss of sports revenue, including at the Toronto Blue Jays. Media adjusted EBITDA decreased by 149% or $107 million, partially offset by lower programming and sports costs associated with the suspension of major sports leagues. Cable revenue decreased by 3% as a result of declines in legacy television and home phone subscriber bases, offset by growth in Ignite TV and internet subscriptions.

Cogeco’s Q3 for the quarter ended May 31 saw overall revenue increase 1.4% to $626.0 million. On a constant currency basis, revenue decreased by 0.6%, explained by a 33% year-over-year decline in radio advertising as a direct result of the COVID-19 pandemic. An increase of 1.1% in constant currency in the Communications segment was recorded, mostly as a result of the American broadband services operations’ growth in both residential and business internet service customers combined with the impact of the Thames Valley Communications acquisition completed on March 10. Adjusted EBITDA increased by 2.9% (1.1% in constant currency) to reach $298.4 million, mostly attributable to higher adjusted EBITDA in the Communications segment due to an increase in the American broadband services operations, partly offset by a decrease in media activities.

Cogeco’s Q3 for the quarter ended May 31 saw overall revenue increase 1.4% to $626.0 million. On a constant currency basis, revenue decreased by 0.6%, explained by a 33% year-over-year decline in radio advertising as a direct result of the COVID-19 pandemic. An increase of 1.1% in constant currency in the Communications segment was recorded, mostly as a result of the American broadband services operations’ growth in both residential and business internet service customers combined with the impact of the Thames Valley Communications acquisition completed on March 10. Adjusted EBITDA increased by 2.9% (1.1% in constant currency) to reach $298.4 million, mostly attributable to higher adjusted EBITDA in the Communications segment due to an increase in the American broadband services operations, partly offset by a decrease in media activities.

Netflix reported global paid net subscriber additions of 10.09 million in Q2, exceeding the 8.26 million expected as people stayed home due to coronavirus. That brings the streaming giant’s total paid memberships to 193 million. Revenues for the quarter came in at $6.15 billion, a year-over-year increase of 25%.

Netflix reported global paid net subscriber additions of 10.09 million in Q2, exceeding the 8.26 million expected as people stayed home due to coronavirus. That brings the streaming giant’s total paid memberships to 193 million. Revenues for the quarter came in at $6.15 billion, a year-over-year increase of 25%.

Corus Entertainment has released an update on the scope and mandate of its ongoing Diversity Review, announced in early June following allegations of a culture of racism and microagressions from a number of current and former employees. The company has engaged the services of anti-racism specialists, DiversiPro, which has initiated interviews with a cross-section of Corus employees on their work experience. That will be followed by a company-wide survey and “intercultural assessments” of 100 senior staff. The last phase of the review will identify any barriers or biases in Corus’ “people-related policies and processes.” Corus said specific recommendations will be presented to the company in a final report this September and integrated into its current Diversity and Inclusion multi-year plan. It says some commitments have already been enacted within the Global News division immediately. Read more here.

ANALYSIS: Brad Danks’ has a second instalment of his series on internet regulation. In Part II, he explores “the content paradox.” Read more here.

ANALYSIS: Brad Danks’ has a second instalment of his series on internet regulation. In Part II, he explores “the content paradox.” Read more here.